How Is My Borrowing Capacity Calculated?

We provide a breakdown of how banks work out how much you can borrow.

Defining what you can afford

Think of your borrowing capacity as a water tank. The bigger your tank, the more founds it can hold – but it’s up to you how much you fill it up.

The maximum you can borrow will be based on your financial situation. To figure this out a lender will calculate your free cash flow, based on money coming in minus money going out. The lender will then evaluate what loan repayments you can afford – and what borrowing capacity or loan size you can realistically take on.

Adding and subtracting

Here’s a more detailed look into what’s evaluated to calculate your free cash flow.

Income

Most commonly, this will be your salary, any bonuses, and rental income if you own an investment property. It could also include things like interest from savings accounts, casual income – like driving for Uber – and dividends from shares.

Debt repayments

Examples of this include, any existing home loan payments, credit card payments, personal or car loan payments, and HECS.

Living expenses

This refers to items like groceries, fuel, clothes, and entertainment. Please note that lenders will generally use the higher of your actual declared expenses or the corresponding Household Expenditure Method (HEM).

Buffer

Due to regulatory requirements, when looking at the interest rates an applicant might be currently paying, we add a buffer – which makes the rate theoretically higher. Here are some common examples.

Credit cards: A buffer of 3.8% of the credit card limit is taken as the monthly debt repayment. This is because – though you might not be using a credit card right now – you might want to at some point. Under this scenario, lenders want to know you can still service all your debts comfortably.

Home loans: Though you may pay 3.00% on your home loan, for assessment purposes the lender will use the higher of your current rate + 2.5% or a floor rate of 5.50%. This is because your home loan rate might change depending on cash rates and how money markets are performing. Lenders want to ensure, when interest rates increase, you’ll still be able to comfortably service your debts.

Certain income: This is money coming in that’s variable or irregular, which will be discounted.

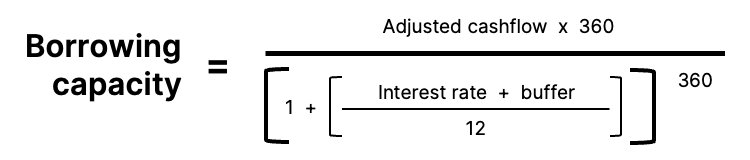

Once your free cash flow is calculated, it’s time to find out your borrowing capacity:

From here, we can see that the longer the loan term, the more you can borrow. That’s because you have more time to pay off the principal. In Australia, the maximum loan term is 30 years. So, assuming you’ll take up a 30-year loan, your borrowing capacity will become:

Here's an example:

Meet Jane, her incomings and outgoings are as follows:

- Monthly after-tax income: $20,000.

- An existing home loan with a $200,000 balance over 25 years on 3.27% interest. The monthly repayment is $977.

- A credit card with a $10,000 limit, and the credit card balance is paid in full every month.

- Monthly living expenses: $3,000.

From here, we can calculate Jane’s free cash flow:

- Income: $20,000.

- Debt repayment: $977.

- Living expenses: $3,000.

- Buffer: $958.

- 3.80% of the $10,000 credit card limit: $380.

- 2.50% additional interest of the home loan: $578.

This means Jane’s free cash flow can be summed up as:

$20,000 - $977 - $3,000 - $958 = $15,065.

Now let’s calculate Jane’s borrowing capacity using a minimum assessment interest rate of 5.50%:

So, there you have it. Based on Jane's financial situation, her borrowing capacity is $1,045,497.

This article is intended to provide general information only. It does not have regard to the financial situation or needs of any reader and must not be relied upon as financial product advice. Please consider seeking financial advice before making any decision based on this information.

Unloan is a division of Commonwealth Bank of Australia.

Applications are subject to credit approval; satisfactory security and you must have a minimum 20% equity in the property. Minimum loan amount $10,000, maximum loan amount $10,000,000.

Unloan offers a 0.01% per annum discount on the Unloan Live-In rate or Unloan Invest rate upon settlement. On each anniversary of your loan’s settlement date (or the day prior to the anniversary of your loan’s settlement date if your loan settled on 29th February and it is a leap year) the margin discount will increase by a further 0.01% per annum up to a maximum discount of 0.30% per annum. Unloan may withdraw this discount at any time. The discount is applied for each loan you have with Unloan.

There are no fees from Unloan. However, there are some mandatory Government costs depending on your state when switching your home loan. For convenience, Unloan adds this amount to the loan balance on settlement.

* Other third-party fees may apply. Government charges may apply. Your other lender may charge an exit fee when refinancing.